Author: Cono Natale

The Sweet Spot

Real Estate markets, like tennis racquets, have sweet spots. When you look at a list of all the listings in your area, you’ll notice that there are bunches in each price range. One group might be those houses priced between $374,000 -$376,000 range while another is comprised of properties in the $390,000 and up range. What you want to do is position your property in an empty spot between those numbers whenever possible. This is called price-banding.

Since the majority of buyers will come to you through the internet first these days, also consider what price range they will be searching for. You might be thinking that the perfect asking price for your home is $305,000, but you’ll be knocking yourself out of the search results for anyone searching in the $250,000-$300,000 range. Far better then, to price yourself within the “century number” so that buyers will find your property included in their search results. A smarter price, in this instance, would be $299,995.

Thursday comic

Thursday comic

The Market You’re Selling Into – Cold, Hot or Neutral? 4 of 4

Finally, a neutral market is exactly what you think it is: A market that is more or less balanced in terms of buyers and inventory. The market you’re in when you list your property should be a factor in your pricing strategy. Essentially then, your property has three different prices. One for a buyer’s market, one for a seller’s market and one for a neutral market. All things being equal, with a list of true comps at $150,000, for example, and leaving a little wiggle room for negotiation, in a buyer’s market, you would price it at $149,900, but expect to sell at $145,000, while in a seller’s market you can ask more than the last comparable sale, up to perhaps $165,000. And, in a neutral market, you might want to set your price at the last comparable sale and then adjust for market trends. So, if the median sales price has edged upward at a rate of 1% per month, you’d be justified to ask for $154,500.

The Market You’re Selling Into – Cold, Hot or Neutral? 3 of 4

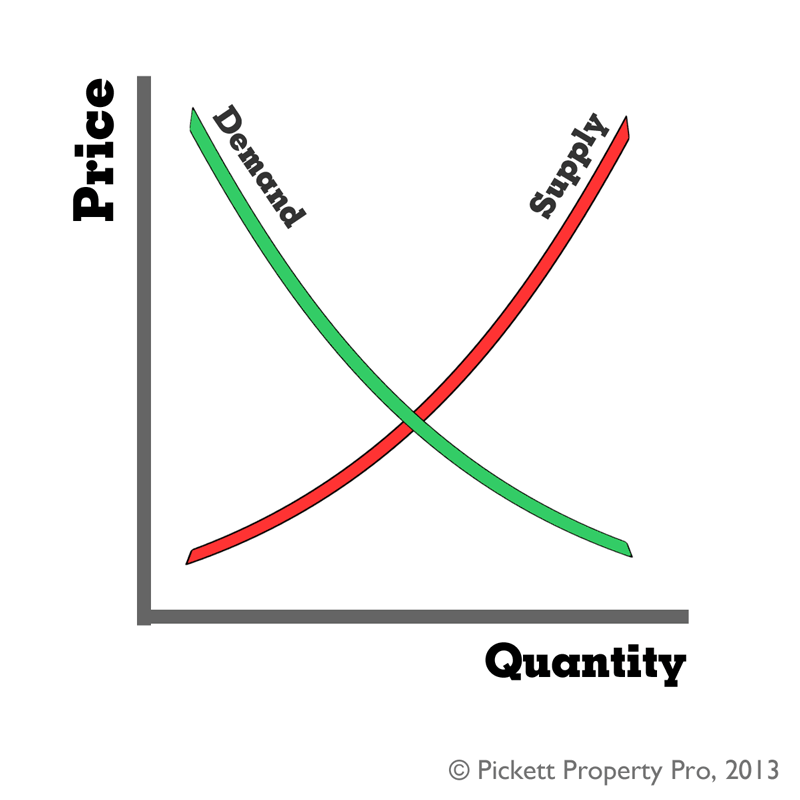

A Seller’s Market, on the other hand, (and may you be so lucky!) is one in which:

Demand is higher;

Less than six months inventory is currently on the market;

Median sales prices are increasing;

Shorter list times;

Multiple offers;

More buyers are purchasing

Thursday comic

The Market You’re Selling Into – Cold, Hot or Neutral? 2 of 4

Basically, a Buyer’s Market is one in which:

Demand is lower;

Inventory is higher;

Longer list times;

Fewer offers;

Price reductions;

More than six months of inventory is on the market (more about this in a moment);

Fewer buyers are purchasing

To calculate inventory accurately, use the following formula: Find the total number of active listings in your market last month. Then find the total of closed and sold transactions from last month. Divide the number of total listings by the number of total sales, which results in the number of months of inventory currently available in your market.

Thursday comic

The Market You’re Selling Into – Cold, Hot or Neutral? 1 of 4